Log In

Log In

Log into Online Banking

Log into Online Bankingby Michelle Bednarski and John Hemak

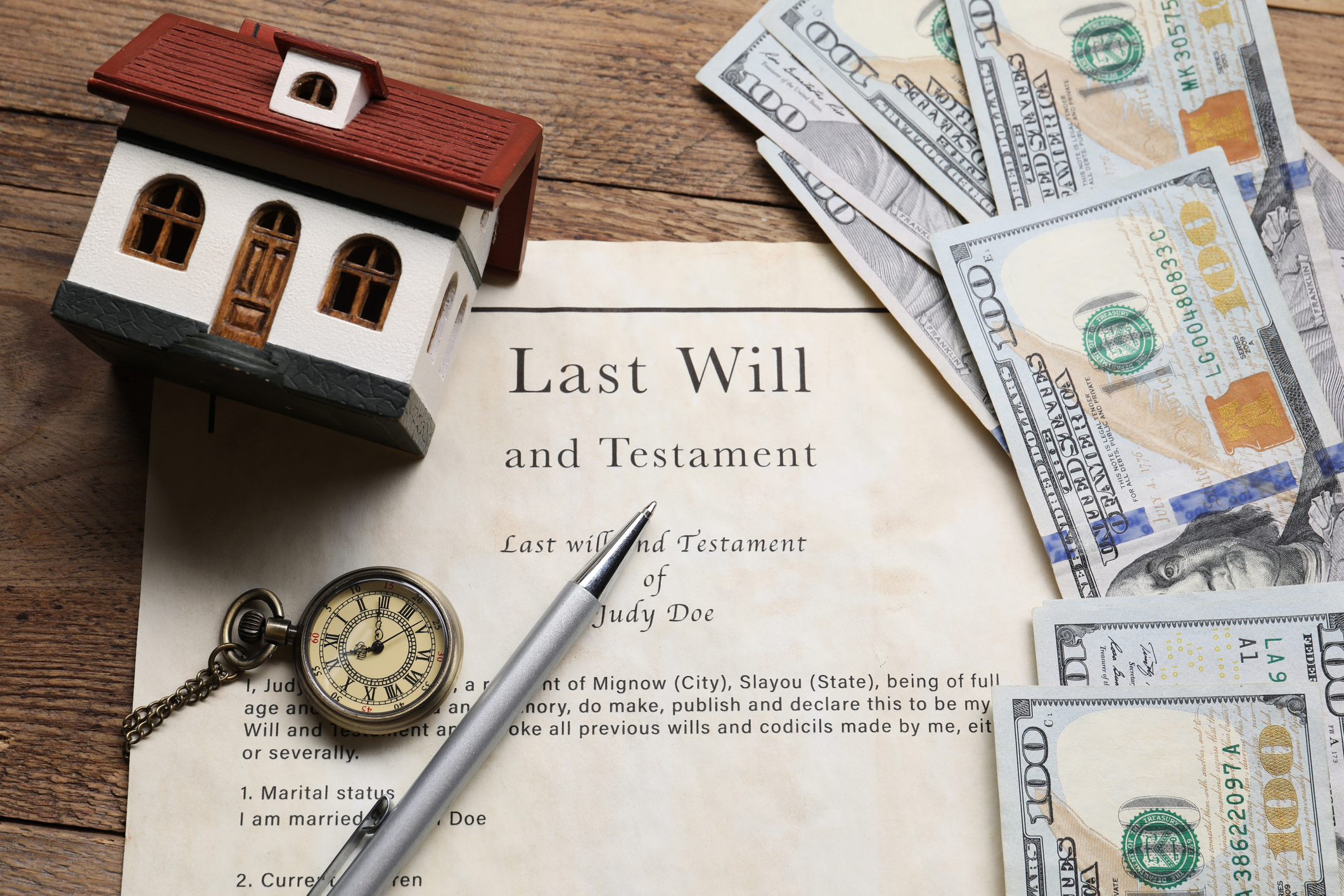

It can be difficult to think about what happens to your belongings after you die. No one likes to think about the end of life, but that doesn’t make it any less important to have a plan in place for when the day comes. Proper estate planning can offer you peace of mind knowing that your assets will be distributed according to your wishes. It also reduces the burden on your loved ones; they can spend the time focusing on grieving and making funeral arrangements and potentially less time settling disputes about your assets.

It can be difficult to think about what happens to your belongings after you die. No one likes to think about the end of life, but that doesn’t make it any less important to have a plan in place for when the day comes. Proper estate planning can offer you peace of mind knowing that your assets will be distributed according to your wishes. It also reduces the burden on your loved ones; they can spend the time focusing on grieving and making funeral arrangements and potentially less time settling disputes about your assets.

Estate planning is a very broad topic, so this article will focus on some of the larger concepts to help you begin to prepare. Working through the following concepts with a skilled estate planning attorney can help to ensure your plan aligns with your wishes.

Assets & Liabilities

Think you don’t have enough wealth to justify estate planning? Think again! When you take the time to create an inventory of your assets, you may be surprised by how much you possess.

There are two types of assets: tangible and intangible. Tangible assets are physical property such as real estate, vehicles, collectibles, and other personal possessions. Intangible assets are financial instruments such as checking and savings accounts, certificates of deposit, stocks, bonds, mutual funds, life insurance policies, retirement plans, and ownership in businesses.

While accounting for your assets, you will also want to list any of your outstanding liabilities. This can include mortgages, lines of credit, and other debts. By having a written list of your liabilities, you can make it easier for your estate’s executor to notify the applicable creditors.

Once you have an idea of your assets, designate your beneficiaries to simplify the process.

There can be a number of legal and financial complexities to consider given your personal situation, but the above steps are a good start in your estate planning process!

Wills

A Last Will and Testament is a legal document which outlines how your assets will be distributed after your death. Without a Will, settling your estate can be a lengthy process with competing parties debating how your assets should be divided. This can cost a significant amount of money and cause undue stress.

To write a Will, there will be certain information that is important to have handy including but not limited to: a full inventory of your assets, a list of beneficiaries for your estate, and detailed instructions for how your belongings are to be distributed amongst these beneficiaries. You will want to designate an executor and also consider designating a successor executor who will use the document to bring your estate through a legal process known as probate, where your estate is settled and distributed.

To write a Will, there will be certain information that is important to have handy including but not limited to: a full inventory of your assets, a list of beneficiaries for your estate, and detailed instructions for how your belongings are to be distributed amongst these beneficiaries. You will want to designate an executor and also consider designating a successor executor who will use the document to bring your estate through a legal process known as probate, where your estate is settled and distributed.

You will also need certain witness and/or notary signatures to validate your Will. The laws surrounding a Last Will and Testament may vary from state to state; you should consider hiring an estate planning attorney to help you ensure the document is legally valid.

Having a Will can help to streamline the process and also can allow for peace of mind in documenting your final wishes.

Power of Attorney

Establishing a Power of Attorney (POA) is an important step in the financial planning process. A POA is a legal document that allows someone to make decisions on your behalf in the event that you are unable to make them for yourself. Depending on the type of POA you have, this can range – to paying your bills and taxes, accessing and managing your assets, or even making healthcare decisions.

There are several types of POA’s available which include the following examples:

- General Power of Attorney – This document grants an agent wide-ranging authority over your legal and financial affairs, including managing bank accounts, buying/selling property, or handling investments. This type of POA remains in effect until you lose mental capacity or in the event of your death.

- Limited Power of Attorney – This document allows you to specify which activities your agent has been granted authority over, typically financial matters. It allows you to set a time period or purpose during which the POA is active. It has narrowly defined powers so that it can be helpful for specific transactions, such as real estate matters, for when you are unable to be present.

- Springing Power of Attorney – This document allows someone to ‘spring’ into effect and make decisions on your behalf only under certain conditions, such as becoming incapacitated or even when you are unable to make decisions for yourself.

- Durable Power of Attorney – This is similar to General Power of Attorney except it remains intact even if you are incapacitated due to illness, injury, or mental decline (for example, being in a coma or under anesthesia).

You should be careful about who you grant power of attorney. Consider assigning medical representation and financial representation to different people, as well as establishing backups for each in case the primary choice is unavailable in an emergency. Choosing someone that you can both trust and who will be able to faithfully carry out the necessary responsibilities in a clear and specific way on your behalf is important. Whoever you choose should be fully aware of their respective responsibilities and your wishes.

Conclusion

Remember that your estate plan can change. Revisiting your estate plan after any major life event, such as marriage, divorce, a sudden increase in wealth, or if any of the people you’ve designated as executors or given power of attorney have passed away should all be a component of proper estate planning.

No one can see into the future, which is why it’s important to plan ahead. Working with a skilled estate planning attorney can help to ensure your plan fully aligns with your wishes.

About the Authors

Michelle Bednarski is the Branch Manager for New Tripoli Bank's Buckeye Office. She has been employed by New Tripoli Bank since 2023 and has worked in various customer-facing positions within the Bank. She is also involved in local business organizations including LeTip of the Lehigh Valley.

Michelle Bednarski is the Branch Manager for New Tripoli Bank's Buckeye Office. She has been employed by New Tripoli Bank since 2023 and has worked in various customer-facing positions within the Bank. She is also involved in local business organizations including LeTip of the Lehigh Valley.

John Hemak is Commercial Lender for New Tripoli Bank and Treasurer of the Board of the East Penn School District Education Foundation. He has been involved in commercial lending for decades and has been a commercial lender for New Tripoli Bank for over 15 years.

John Hemak is Commercial Lender for New Tripoli Bank and Treasurer of the Board of the East Penn School District Education Foundation. He has been involved in commercial lending for decades and has been a commercial lender for New Tripoli Bank for over 15 years.

Buying a home is likely the most expensive purchase you’ll make in your lifetime. It takes years of planning, sacrificing, and saving just to get the keys to your first home. Even after you’ve signed all the paperwork and paid the closing costs, home ownership expenses don’t stop at financing.

Buying a home is likely the most expensive purchase you’ll make in your lifetime. It takes years of planning, sacrificing, and saving just to get the keys to your first home. Even after you’ve signed all the paperwork and paid the closing costs, home ownership expenses don’t stop at financing.

Many homebuyers fail to account for the expenses that come after they’ve moved in. Things like taxes and insurance are the obvious, but there’s also the hidden cost of routine repairs and maintenance that many never consider.

However, there are several ways you can lower everyday homeownership costs that will help balance your budget and can potentially increase the value of your home in the process. Here are some tips to save money as a homeowner!

Make Your Home More Energy Efficient

Many homeowners end up spending more than they need on energy bills purely due to a lack of knowledge about how to make a home energy efficient. One of the simplest ways to reduce your energy bills is to install energy-efficient light bulbs. You should also get into the habit of switching off outlets when not in use.

You can go one step further and install energy-efficient appliances. While these purchases will cost you a bit up front in the short term, they can save you greatly in the long run. New Tripoli Bank can help you finance your new appliances by taking advantage of your equity in your home with a Home Equity Line of Credit.

Updating your appliances with newer, more energy-efficient models can actually increase the value of your home, if you are considering reselling in the next few years!

Shop Around for Homeowners’ Insurance

Lenders require you to have homeowners’ insurance arranged before you close on your house. Most homebuyers tend to purchase their homeowners’ insurance and then never consider it again. However, shopping around for quotes on your homeowners’ insurance is a great way to find better premiums and potential savings.

This is also a great time to consider how much insurance you need. What kind of coverage do you realistically need? Can you afford a higher deductible? Take stock of your belongings and consider what makes sense for your situation.

Regular Maintenance & Repairs

Regular Maintenance & Repairs

Staying on top of home maintenance can help you save money in the long run and prevent bigger, costlier problems from occurring. Fixing issues when they only involve small repairs or performing regular maintenance is easier and cheaper than waiting until the problem turns into a major issue. Regular home maintenance can also increase your energy efficiency, helping to reduce your monthly utility bills.

You can save even more money by doing your own maintenance. Home appliances come with manufacturer’s use and care booklets with guides on how to repair common issues and keep your appliances clean and functioning. You can also find information on home maintenance at your local library or through DIY videos on YouTube, though in the case of the latter you should be careful to get your information only from knowledgeable, experienced sources.

When all else fails and a repair or maintenance job is beyond your capabilities, make sure you comparison shop for the best contractor for the job. This does not necessarily mean the cheapest professional. Again, you should make sure the person you hire for the job is experienced and isn’t cutting corners in a way that could lead to further costly issues in the future. Check with organizations like the Better Business Bureau or review feedback on sites like Yelp or Google to make sure that the business has good reviews from previous customers.

Conclusion

While buying a home is expensive, maintaining it doesn’t have to be. You can save money with a few simple tricks and potentially increase the value of your home in the process.

If you are looking to finance home repairs or improvements, you should reach out to New Tripoli Bank. We have several options to help you pay for home maintenance, whether it’s a dedicated Savings Account to set up an emergency fund for potential future repairs, or a Home Equity Line of Credit to pay for appliance replacements.

Donna Sigley is a Vice President and Mortgage Loan Officer with New Tripoli Bank and has been a part of the New Tripoli Bank team for over 25 years. She has helped several home owners achieve financing for their homes and has decades of experience in mortgage financing. When she's not busy working for the Bank, she's enjoying the outdoors and spending time with her husband, family, and friends.

Donna Sigley is a Vice President and Mortgage Loan Officer with New Tripoli Bank and has been a part of the New Tripoli Bank team for over 25 years. She has helped several home owners achieve financing for their homes and has decades of experience in mortgage financing. When she's not busy working for the Bank, she's enjoying the outdoors and spending time with her husband, family, and friends.

When it comes to personal finance, many consumers express a desire to save more money but struggle to stick with a savings plan. Life is filled with expenses, temptations, and surprises, all of which can make it difficult to maintain consistent banking habits. This can lead to unexpected overdraft fees and missed payments, which increases your stress levels and impedes your ability to build your personal wealth.

When it comes to personal finance, many consumers express a desire to save more money but struggle to stick with a savings plan. Life is filled with expenses, temptations, and surprises, all of which can make it difficult to maintain consistent banking habits. This can lead to unexpected overdraft fees and missed payments, which increases your stress levels and impedes your ability to build your personal wealth.

Consistency is a fundamental building block toward financial wellness, and one of the simplest and most effective ways to remain consistent with your money habits is to automate your banking. Implementing automation strategies and digital payments can help reduce your mental workload by creating a system that handles income, recurring payments, and savings while keeping your hands off your finances to reduce the temptation for impulse spending.

Here are steps you can take to automate your banking.

Automate Your Income

Direct deposit has become the standard method for receiving paychecks, but there are additional steps you can take to further automate your income in a way that makes it easier to save. If your employer allows it, you should consider splitting your direct deposit between multiple checking and savings accounts based on your budget. For example:

- You deposit 50% of your paycheck into a savings account dedicated to monthly expenses.

- You deposit 30% of your paycheck into a checking account for discretionary spending.

- You deposit 20% of your paycheck into a savings account for long-term savings and debt repayment.

This strategy relies on you knowing how much money you’ll need for each category in a pay period, so you'll need to determine your budget beforehand. If your employer doesn’t offer a direct split, you can mimic this strategy by setting up automated scheduled transfers each payday from whatever account receives your direct deposit.

Set Up Automatic Bill Pay

Missing a bill payment can happen to even the most organized consumer. To avoid this and the associated fees in the future, you should consider enabling automatic bill payments or debits.

Most banks have automated bill payment tools that allow you to set up recurring payments to vendors, and many vendors offer automatic payment options that will connect your account with that vendor to your bank account so you can enable automatic monthly transfers. This is useful for recurring payments such as rent, mortgage payments, utilities, insurance, and credit cards.

Keep in mind that once automatic transfers are set, it can be easy to forget about them! Make sure that you have a dedicated deposit account for recurring payments and ensure that you deposit enough money into that account each pay period to cover your monthly expenses. This will help prevent overdrafts and keep your spending separate from your obligations.

New Tripoli Bank’s online banking tools include a Pay My Bill feature that allows you set up automatic monthly payments from your deposit account. This is a 100% free service that allows you to control your bill payment schedule.

Pay Yourself First

Pay Yourself First

Most people try to save by waiting to see what’s left after their monthly expenses. Unfortunately, human nature makes consumers more likely to spend money when it’s sitting in our checking account, and advertising is designed to encourage us to spend before we think. By the time you’re done paying bills, buying necessities, and spending money on things you want, there can be little left to save.

This is why it’s important to save automatically whenever you receive your paycheck. You should have a dedicated savings account for your long-term savings and set up automated transfers into that account on each payday to ensure some percentage of your income is put toward long-term savings goals.

Bank Account Alerts

Sometimes, unforeseen circumstances can lead you to overdraft on your account. This can be something as innocuous as two bill payments lining up at the wrong time, or as serious as unauthorized transactions on your account due to fraud. It’s important that you keep abreast of your finances even when automating your banking.

Enabling alerts for all of the automated transactions we’ve discussed so far can help you avoid unnecessary fees. When it comes to money transfers, account alerts indicating a low balance can help you decide if an automatic payment or transfer should be rescheduled to avoid overdrafts or late payments.

Beyond opting into overdraft account and unusual activity messages, other alerts to consider turning on include:

- High balance alerts to remind you to move extra money into your long-term savings or to pay down debts.

- Direct deposit alerts to help you determine when you should time larger purchases or schedule regular bill payments.

- ATM withdrawal alerts to let you know when your checking account might be slimmer than expected, which is especially helpful for those with joint accounts.

The Bigger Picture

When your bank account is automated, your financial life becomes much more predictable. You spend less time worrying about money and more time using it intentionally. Operating from a plan ensures that you’re not constantly reacting and causing undue stress. Over time, these small, automated actions compound into a larger plan of building wealth.

New Tripoli Bank’s online banking platform with card management, alerts, and automated bill pay is the perfect tool to help you accomplish your financial goals. If you’re already a customer, you can get started by logging into our online banking tools. If you’re not yet a customer, you can call us to learn more or open your own bank account here and start accessing our personal digital banking services today!

Jen Moyer is Vice President and head of New Tripoli Bank's Deposit Operations. She has been a member of the New Tripoli Bank team for over twenty years and has worked in multiple departments within the Bank.

by Carissa Fallon

Establishing and building credit is an essential component of financial health, influencing everything from financial milestones to long-term goals. This article will provide insight into how you can build credit, establish a monthly budget, manage your debt responsibly, and understand what elements are used to determine your credit score.

Ways to Build Credit

As a young adult, I established and then built my credit by getting my own credit card as I was heading to college. However, each person’s path is different. Some of you may build your credit by obtaining an auto loan or applying for a student loan. Another way to build credit is by being added as an authorized user on a family member’s credit card. Just make sure that they are in good standing; being an authorized user on the credit card of someone with poor credit can actually negatively impact your credit score.

A credit card is an example of “revolving credit”. This means that you are able to utilize funds up to a certain limit, repay them in accordance with their terms/conditions, and then use them again without the need to reapply, with the understanding that your account remains in good standing. For example, if your credit card limit is $1,000, you can’t spend more than $1,000 in a month (or statement period) on your credit card. Once you pay down or pay off your balance, you can spend again the following month. However, your payment amount may vary depending on the statement ending balance and other factors such as interest.

Student and auto loans are examples of “installment loans”. An installment loan allows you to borrow a lump sum of money and pay it back over a period of time through “fixed” monthly payments. For example, most student loans are paid back over the course of 10 to 20 years, whereas an auto loan can range from 24 to 84 months. Both instances have a fixed principal and interest payment for the duration of the loans. A fixed monthly payment can help to budget for that payment.

Once you determine which credit building method is best for you, it is important to create a monthly budget, so you are aware of your income and expenses and can avoid spending outside of your means.

Creating a Budget

Creating a budget is pivotal for your financial success. It is important to know how much money you are bringing in and where it goes once you get it. You can create a budget using Google Sheets, Microsoft Excel, or even using a pen/paper. Whichever way it is easiest for you to create a budget, you’ll need to know your expected monthly income and then all of your typical expenses.

A budget will help you understand how your money is spent and gives you the opportunity to adjust, such as cutting spending or using money to invest. Managing your money effectively is important because it will help you reach future financial milestones.

Manage Your Debt

Once you have obtained a credit card, student loan, installment loan, or other debt, you should familiarize yourself with the payment schedule so you can ensure timely payments. Setting up automatic payments is extremely helpful and can help to prevent fraud. You just need to make sure you keep enough money in your account at the time that the payments are due each month. Additionally, it is good to get into the habit of checking your monthly statements to ensure that each transaction on your account is authorized and no fraud has taken place.

A great way to start using your credit card would be putting a monthly subscription such as Netflix, Spotify, or other reoccurring payment onto a credit card and then connecting your checking account to the card to pay in full each month. This single monthly payment will start building your credit, even though it is a smaller amount. Once you get more comfortable with your budget, you can consider using your credit card more often. Be sure to only spend what you can afford to pay back, so you can stay on top of your payments and continue to build good credit.

Similarly for an installment loan, ensuring that the payment is made on time each month will help build your credit over the duration of the loan.

After you have established and built your credit, you should understand what elements are used to determine your credit score as part of your overall credit report and how it can impact your financial health over time. Mistakes can happen, so it’s important to monitor and subsequently understand your credit report and what is included so you can dispute such inaccuracies.

Conclusion

Building a good credit score is a process that takes time, which is why it’s important to start early! For those of you headed to college, talk to your parents or guardian about becoming an authorized user on their credit card to pay for stuff like school supplies and groceries. The sooner you start building up credit, the more likely you’ll have a solid credit score when the time comes to apply for credit on your own.

And remember, you can always talk with a lender at New Tripoli Bank. Stop in or give us a call - we are happy to help!

Carissa Fallon is a Loan Administration Specialist for New Tripoli Bank. She graduated with honors from Penn State University with a Bachelor of Science in Finance. When she's not working, she enjoys playing tennis, spending time with her family, and keeping an active lifestyle.

Carissa Fallon is a Loan Administration Specialist for New Tripoli Bank. She graduated with honors from Penn State University with a Bachelor of Science in Finance. When she's not working, she enjoys playing tennis, spending time with her family, and keeping an active lifestyle.

Ask anyone still working in their 50s and 60s about their plans for retirement, and you’ll often receive responses about places they want to go, hobbies they plan to get into, and how much free time they’ll have. However, that’s only half of the story when it comes to retirement. In order to take that trip to Peru or get really into soap carving, you’ll need to have a plan for how you’ll pay for everything once you’re no longer receiving a paycheck.

Ask anyone still working in their 50s and 60s about their plans for retirement, and you’ll often receive responses about places they want to go, hobbies they plan to get into, and how much free time they’ll have. However, that’s only half of the story when it comes to retirement. In order to take that trip to Peru or get really into soap carving, you’ll need to have a plan for how you’ll pay for everything once you’re no longer receiving a paycheck.

The truth of the matter is: you don’t have to wait until your super wealthy to retire. You just need to ensure you have enough money to get by. Once you no longer need to worry about going broke or paying for medical expenses, you can start focusing on ways to improve your life satisfaction.

So, let’s talk about how you achieve that goal.

Plan Ahead

Circling back to the start of this article: what are your plans for retirement? Ask yourself if you want to travel, whether you’d like to move to a new house, if you plan on working part-time or if you want to spend your time volunteering in local organizations. How you plan to spend your retirement will help inform how much you need to save to achieve the retirement you want.

In addition to the “fun” things you want out of your retirement, you also need to take into account that you’ll need to pay for medical expenses, food, gas, taxes, and debts.

Think about how much you spend right now on these things and determine if you want to cut back on your standard of living. Most of your day-to-day expenses will remain the same, but things like commuting costs, dining out and clothing may change depending on your situation.

Once you have an idea of your expenses, realize that you will need to pay for these expenses through a combination of annuities from your retirement savings, investments, and Social Security. This gives you a target number that you can use to plan out your retirement saving strategy.

Start Early

There is a quote often attributed to Albert Einstein that “the most powerful force in the universe is compound interest.” While the origin of this quote is debated, it reflects the importance of starting early when it comes to saving. Interest compounds over time, so the sooner you begin putting money into a retirement account, the more time you have to take advantage of the effects of compound interest.

Explore Your Options

Explore Your Options

If you haven’t already, consider opening up an Individual Retirement Account (IRA) to start putting money into it. Determine how much you can contribute from each paycheck to your retirement account and set up automated recurring contributions to ensure that a portion of your income is allocated to your retirement fund. This takes out the temptation to skip contributions and makes the process less stressful.

There are different types of IRAs you can choose from, each with its own benefits and drawbacks. You should consult your financial advisor or IRA specialist to help you determine what is best for your situation.

You should also check with your employer to see if they offer a 401(k) benefit. These accounts are similar to IRAs but the funds are automatically taken out of you paycheck and many employers offer matching contributions, which is essentially free money.

Increase Your Contributions (When You Can)

It can be tempting to “set it and forget it” when it comes to retirement savings. Our brains are wired to be more concerned with the here and now than to worry about our future. But as circumstances change, whether it be an increase in your standard of living or a change in priorities, you should make a point to periodically revisit your retirement strategy.

You should revisit your contributions if your current situation improves to the point that you can comfortably increase the amount you’re putting away each month. Your goal should be to eventually reach the IRA contribution limit and max out your yearly contributions to ensure you have a comfortable nest egg when you retire. Individuals age 50 or older, there is also a “catch up” amount that allows you to contribute even more to your retirement.

Conclusion

Retirement is a major transition made up of many financial and life decisions. The choices you make now will impact how comfortable you are when it comes time to retire.

You might also want to consider regularly updating your retirement plans and seeking the professional guidance of a financial adviser. That way, you can spend more time focusing on everything else that matters.

Jenna Smith is an Assistant Vice President and the Branch Manager for New Tripoli Bank's Claussville Office, as well as a certified IRA Services Professional who has worked for New Tripoli Bank since 2006. She completed the PA Bankers Advanced School of Banking and has been helping customers for many years. She has dedicated her career to learning all she can about banking and finance and in her free time enjoys spending time with her family and working on arts and crafts.

Jenna Smith is an Assistant Vice President and the Branch Manager for New Tripoli Bank's Claussville Office, as well as a certified IRA Services Professional who has worked for New Tripoli Bank since 2006. She completed the PA Bankers Advanced School of Banking and has been helping customers for many years. She has dedicated her career to learning all she can about banking and finance and in her free time enjoys spending time with her family and working on arts and crafts.

Tax season is here! While that might not be the most exciting news for the average person, it’s important to keep the following in mind so that filing your tax return is a smoother and less tedious process. You may also be able to save a little time and money in the process!

Tax season is here! While that might not be the most exciting news for the average person, it’s important to keep the following in mind so that filing your tax return is a smoother and less tedious process. You may also be able to save a little time and money in the process!

Save the Date

First of all, a quick reminder that your tax returns are due April 15th. If you think you need more time and want to avoid a failure-to-file penalty, you will need to fill out IRS Form 4868 (Application for Automatic Extension of Time to File U.S. Individual Income Tax Return) by April 15th. Remember that this does not typically give you an extension on paying your taxes, as your estimated tax liability payment is still due by April 15th!

Direct Deposit Is Your Friend

If you think you may be entitled to receive a refund, you should consider setting up direct deposit. Electronically filing your taxes and choosing direct deposit is the fastest way to get your refund. When utilizing direct deposit, the IRS issues over 90% of refunds in less than 21 days of filing. Refunds from paper filings can take up to 6 to 8 weeks from the date the IRS receives your return.

Direct deposit also provides improved security by avoiding the mail, which can leave your refund susceptible to mail fraud.

If you don’t have a bank account, you should consider opening a no-cost personal checking account in order to set up direct deposit when you file. New Tripoli Bank’s personal checking account has no minimum balance requirement to open and no monthly maintenance fees. Setting up a new account can be done easily online or at one of our local branches. Please let us know how we can best help you.

Check for Free Options to File

Certain individuals are eligible to have their basic tax returns prepared and filed for free, allowing them to save time and money. Available options to consider include the AARP Foundation Tax-Aide, the IRS’s Tax Counseling for the Elderly (TCE) programs, and the IRS’ Volunteer Income Tax Assistance (VITA) program, which connect consumers with IRS-certified tax preparers.

Also, if your adjusted gross income is $89,000 or less, you are eligible to prepare and file your income tax returns for free online through the IRS Free File portal.

Active-duty service members, retired and honorably discharged veterans, family members managing the affairs of eligible service members, and survivors of deceased service members can prepare and file their tax returns for free through MilTax.

Guard Against Fraud

Tax season is a prime time for scammers looking to prey upon the confusion of tax filers. Remember that the IRS will never initiate contact with taxpayers via email, text messages, or social media channels to request personal and financial information.

If you plan to pay a tax preparer to help file your taxes, make sure to check the preparer’s qualifications before handing over any personal or financial information. You can use the IRS directory of federal tax return preparers to check their credentials and verify their information with the Better Business Bureau. Be wary of a preparer that makes guarantees about getting larger refunds, asks you to pay with cryptocurrency or even gift cards; these could be signs of a scam.

Conclusion

You should consult a tax professional for any questions you may have. Depending on your individual situation, their guidance can be instrumental in having your return filed accurately as well as getting you the maximum refund you are entitled to. There are many free options available and I hope that the tips laid out in this article will help you have a less stressful tax season this year!

Matthew Koncz is New Tripoli Bank's Controller and an Assistant Vice President. He has been with the Bank for over seven years and is responsible for monitoring New Tripoli Bank's financial health. He is also a Certified Public Accountant and has completed educational programs for CPAs offered by various accounting firms and organizations including PA Bankers.

Matthew Koncz is New Tripoli Bank's Controller and an Assistant Vice President. He has been with the Bank for over seven years and is responsible for monitoring New Tripoli Bank's financial health. He is also a Certified Public Accountant and has completed educational programs for CPAs offered by various accounting firms and organizations including PA Bankers.

by Kayla Schnellman

Do you believe in reinvesting in your community, but are struggling with how to put that into action? One surefire way is to do business with a community bank. Who you choose to bank with matters just as much as which stores you choose to shop at.

Community Banks Strengthen the Local Economy

If you’ve ever wondered if it matters where you deposit your hard-earned money, let me assure you it does. Not only does banking locally support small businesses (community banks fund nearly 60% of small business loans and more than 80% of agricultural loans), but as locally owned and operated businesses themselves, they are part of the economic engines that have powered 63% of net jobs created since 1995.

Community banks like New Tripoli Bank use your deposits to distribute loans that feed into a self-sustaining micro-economy that keeps funds in the Lehigh Valley. Moreover, community banks reinvest your dollars into the community through donations and sponsorships for local organizations and nonprofits. It is all part of a symbiotic relationship that community banks have with their communities. And the proceeds from those businesses create jobs, fund municipalities, and continue the cycle of locally based economic growth.

Consider the community bank impact on local communities:

- Community banks’ net satisfaction score topped large banks by 13 points, finance companies by 25 points, and online lenders by 60 points.

- 70% of community bank loan applicants were satisfied with their experience, compared with 59% at large banks, 50% at finance companies, and 28% at online lenders.

- Community banks operate in areas abandoned by others—serving as the only physical banking presence in nearly one in five U.S. counties.

Community Banks Offer Personalized Service

Community Banks Offer Personalized Service

The choice to do business with a community bank is not just about the broader economy. When customers contact New Tripoli Bank, they are greeted by a talented team member who is attuned to their respective needs.

Community banks like New Tripoli Bank believe in building strong, long-term relationships with our customers through reliability, flexibility and goodwill. Because community banks serve a smaller geographic area than national banks, they are able to provide more flexible lending options for consumers and businesses, often assessing the broader picture of a person or organization’s financial situation, rather than just basing decisions off automated information, like credit scores.

Further, community banks also put a greater emphasis on maintaining long-standing relationships with their core depositors. While larger financial institutions seem to constantly change their service offerings in reaction to market trends, community banks focus on stability and reliability, which allows for them to plan for the future confidently. Making strategic decisions regarding lending and expansion is a component of that focus. This is one of the main reasons New Tripoli Bank has remained independent for 116 years.

Conclusion

We want to thank our customers for putting their trust in us for their banking needs. At New Tripoli Bank we pledge to never lose sight of the all-important relationships we hold and the personalized service our customers expect. Community banks are only successful if our customers and communities are, too. That’s why community banks and our relationship-based business model have thrived for over a century.

We know what it takes to create successful local economies. Join us in helping to build a vibrant economy here at home, in our community. We look forward to serving you soon.

Kayla Schnellman is the Client Services Lead for our New Tripoli Office. She has worked for New Tripoli Bank for over seven years, where she has worked as Community Banker, Customer Service Representative, and Head Teller. When she's not working, she enjoys spending time with friends and with her three dogs.

Kayla Schnellman is the Client Services Lead for our New Tripoli Office. She has worked for New Tripoli Bank for over seven years, where she has worked as Community Banker, Customer Service Representative, and Head Teller. When she's not working, she enjoys spending time with friends and with her three dogs.

by Tanya Hausman

I often spend time thinking about the best ways to prepare my children for the responsibilities of adulthood. Whether it’s teaching them the importance of proper hygiene, helping them learn how to manage their time between homework and social time, or encouraging healthy eating habits, I understand how vital it is that I be involved in their development.

One of the worries that I have personally experienced as a parent comes from my children having a debit card. Parents or guardians who have experienced a child begging for a brand-new iPhone or asking for money to go out with friends want that child to learn how to save money and spend it responsibly. Debit cards come with potential security risks on top of requiring some level of financial literacy.

Here are some tips to consider before letting your child have their own debit card.

Set Clear Rules

Before handing over the debit card, establish concrete guidelines for its usage. Discuss spending limits and clarify when and where you are comfortable with the card being used. Emphasize the importance of your child regularly checking their account balance before making a purchase.

Setting these rules in place at the start ensures less confusion later on.

Open a Linked Account

The best way to keep an eye on their spending habits is to link their checking account to your online bank account. This allows you to set spending limits and ATM access for children who are just starting to handle their own money, which gives them the freedom to use their debit card while putting restrictions in place.

Consider linking their account to your personal online banking account as it will also allow you to set up transfers between your other accounts and your theirs, making it easy to move money they earn from chores, allowance, etc. If they have a job, you can help them set up direct deposit into their account.

New Tripoli Bank customers can bring their children to any of our branches, and we’ll help to set all of this up!

Monitor Their Activity

Teaching children financial literacy and proper debit card use is a commitment towards long-term success. Once they have their own debit card, you’ll likely want to keep an eye on how they’re spending money. If you see them spending every dollar as soon as they get it, sit down with them and explain the importance of saving money for long-term goals, emergencies or just items that are important to them.

New Tripoli Bank’s online banking platform can help in this regard. You can add your child’s debit card to your account’s Card Secure and set up push or email notifications, so you are alerted whenever your child uses their card. Among other features, it also allows you to set restrictions on the card or deactivate it.

Teach Good Money Habits

It’s not enough to give your child the keys to their own finances; you need to show them how responsible adults budget their money. Most of a child’s learning comes from imitating those in their “money circle,” so it’s important to teach good habits.

Plan your monthly budget together. It’s important for children of all ages to learn concepts like income, expenses, and saving. If you’re currently saving up for a long-term goal, take the time to explain the budget process. Talk about how much you set aside each month, how you decided on that number, where you cut your other spending to save, and emphasize the importance of saving for the future.

Emphasize Security

A big part of using a debit card is making sure your personal and bank account information is secure. It’s critical they choose a strong, unique PIN for their debit card and go over emergency protocols in the event that the card is ever lost or stolen.

Customers at New Tripoli Bank can use the Card Secure feature on our online banking platform to monitor card activity. Take the time to go over their monthly bank statement together and explain how they can proactively identify potentially fraudulent transactions on their account in a timely manner.

Teach them the importance of online safety, whether it’s only buying from secure websites (look for “https” in the URL and a padlock symbol), avoiding entering personal information while on public Wi-Fi, or being able to identify scam ads and fraudulent offers on open marketplaces such as Facebook Marketplace.

Learning Through Experience

Mistakes on their journey to adulthood are likely. Use these mistakes as teachable moments instead. For example: if they overspend, spend some time talking about how it’s important to keep track of their account balances and avoiding impulse purchases.

As they become more comfortable using their debit card and show responsible habits, consider gradually loosening the controls you have on their card. This helps build trust between both of you and at the same time encourages them to continue practicing smart spending habits independent of your monitoring.

Tanya Hausman is a Senior Deposit Operations Specialist at New Tripoli Bank. She has been working for the Bank since 2014 in various roles. Outside of work, she spends her time baking, hobbying, and raising her two children.

Tanya Hausman is a Senior Deposit Operations Specialist at New Tripoli Bank. She has been working for the Bank since 2014 in various roles. Outside of work, she spends her time baking, hobbying, and raising her two children.

Effective immediately, we are unable to accept loose or wrapped pennies due to the Federal Reserve Bank restricting the supply of pennies.

The U.S. Department of the Treasury has officially ended production of the penny, which means New Tripoli Bank can no longer order pennies from or ship pennies to the Federal Reserve. We understand that this change will impact all of our customers and wanted to provide information on this shift in our monetary system.

Here are the main ways this change will impact our customers:

- We may not be able to do change orders that include pennies.

- You may be required to deposit your check if the change back to you would require pennies. You can then withdraw the cash that you need.

- For non-customers cashing a check drawn on New Tripoli Bank, you may be required to open an account if the change back to you would require pennies (exceptions may apply).

- Retailers and businesses may begin rounding cash transactions to the nearest nickel as pennies become unavailable.

Why is penny production ending?

The decision stems from the rising costs to produce new pennies. The current cost of the materials to create a new penny is almost four times the value of the currency, which in turn costs the government money each year.

Even though pennies are no longer being produced, existing ones are still legal tender. Here are some smart ways to transition away from using pennies:

- When paying cash at retailers, expect totals to be rounded to the nearest five cents.

- Consider switching to using digital payments or your debit card, which remain unaffected by the change.

- Sign up for direct deposit for paychecks and government benefit payments.

Every parent or guardian knows one of the most effective methods for motivating kids to do something boring is to turn it into a game. For example: assigning points values to household tasks like cleaning up their bedroom, putting away their toys, or taking out the trash, with the promise of a reward when the child reaches a certain point total.

Every parent or guardian knows one of the most effective methods for motivating kids to do something boring is to turn it into a game. For example: assigning points values to household tasks like cleaning up their bedroom, putting away their toys, or taking out the trash, with the promise of a reward when the child reaches a certain point total.

This is referred to as “gamification,” where you take the most engaging elements of a game, such as competition and rewards, and apply them to real-life activities. Gamification can help make otherwise mundane tasks feel less like chores by tapping into the human desire for achievement.

Gamification can be equally useful for adults trying to establish good spending habits. You can “trick” your brain into positive behaviors by attaching a reward to that behavior. Whether you’re looking for ways to teach your kids financial literacy or want to motivate yourself to get your finances in order, here are some ways you can gamify your savings.

Level Up Your Saving with Short-Term Rewards

Saving money is hard. At a basic level, you are depriving yourself of present gratification to save for a future goal. We’ve all heard of retail therapy; our brains are wired for the dopamine rush that comes from getting what we want, which leads many to spend their money as soon as they receive it (and sometimes even before then). However, we can use this chemical impulse to our advantage!

Setting up short-term, budget-friendly rewards for reaching savings thresholds can help alleviate this habit by providing you with small dopamine rushes along the path to your eventual savings goal. For example, let’s say you are trying to save up $1,000. You create a rule that, for every $200 you save towards this end goal, you will treat yourself by going out to a restaurant for lunch. Suddenly, saving that $1,000 becomes a series of “level ups” that you need to reach to “finish” your game, and along the way you get to enjoy the rewards of hitting each milestone.

One of the benefits of this strategy is that it requires you to pay attention to your income, which is an essential habit for anyone learning how to budget properly. You can maintain a better sense of your financial situation and become more mindful of the connection between your money and the time it takes for you to earn it.

Utilize Visualizations

Most people who have participated in a fundraiser will have seen an example of this strategy. Fundraising organizers use an oversized cardboard thermometer to represent the amount of money that has been raised, to provide a visual shorthand of the progress being made. By displaying the distance from the goal and seeing the shrinking gap between your current progress and the target, it helps you understand your progress at a glance and encourages you to continue as you get closer to your goal.

There are many savings apps that provide interactive charts, graphs, and other visual trackers to help turn numbers into easier-to-read visual data. These apps can also provide real-time updates and notifications to remind users of their achievements, which can also reinforce their motivation to save.

Engage in Friendly Competition

Engage in Friendly Competition

While it can feel awkward discussing money issues with friends, sometimes having a support network around you is the best way to encourage saving. You should consider participating in a savings challenge with friends or relatives to encourage everyone to practice good spending habits. If you do decide to go this route, make sure to keep the competition friendly! Compete for bragging rights rather than material rewards.

You should consider creating a physical leaderboard that you can update periodically to show who is in the lead in your competition. This kind of challenge also encourages participants to share their progress, tips, and success stories with one another, as well as providing a support network in case certain participants are struggling to hit their savings goals.

Ready, Set, Save!

Introducing gamification into your personal finances can help you develop consistent savings habits. Our brains love completing challenges and earning rewards, but sometimes it can feel like saving money isn’t a reward in itself and you need that little extra push to get you into the habit.

Whatever it is you decide to do, the key is to get started and stick with your plan!

If you’re having trouble figuring out how to get started, reach out to a customer service representative at your financial institution. If you’re looking for a change in financial institution, New Tripoli Bank’s team of community bankers are trained to help individual customers who might need assistance when it comes to reaching financial goals, and we are constantly updating our online and mobile banking platforms to provide customers with the tools they need to practice good spending habits.

Kate Hart-Zayaitz is New Tripoli Bank's Chief Lending Officer and Senior Vice President. Kate has spent many years working for various community banks in our area. She was born and raised in Emmaus and has been involved with multiple banking and economic organizations throughout the Lehigh Valley.

Kate Hart-Zayaitz is New Tripoli Bank's Chief Lending Officer and Senior Vice President. Kate has spent many years working for various community banks in our area. She was born and raised in Emmaus and has been involved with multiple banking and economic organizations throughout the Lehigh Valley.