Log In

Log In

Log into Online Banking

Log into Online Bankingby Kayla Schnellman

Do you believe in reinvesting in your community, but are struggling with how to put that into action? One surefire way is to do business with a community bank. Who you choose to bank with matters just as much as which stores you choose to shop at.

Community Banks Strengthen the Local Economy

If you’ve ever wondered if it matters where you deposit your hard-earned money, let me assure you it does. Not only does banking locally support small businesses (community banks fund nearly 60% of small business loans and more than 80% of agricultural loans), but as locally owned and operated businesses themselves, they are part of the economic engines that have powered 63% of net jobs created since 1995.

Community banks like New Tripoli Bank use your deposits to distribute loans that feed into a self-sustaining micro-economy that keeps funds in the Lehigh Valley. Moreover, community banks reinvest your dollars into the community through donations and sponsorships for local organizations and nonprofits. It is all part of a symbiotic relationship that community banks have with their communities. And the proceeds from those businesses create jobs, fund municipalities, and continue the cycle of locally based economic growth.

Consider the community bank impact on local communities:

- Community banks’ net satisfaction score topped large banks by 13 points, finance companies by 25 points, and online lenders by 60 points.

- 70% of community bank loan applicants were satisfied with their experience, compared with 59% at large banks, 50% at finance companies, and 28% at online lenders.

- Community banks operate in areas abandoned by others—serving as the only physical banking presence in nearly one in five U.S. counties.

Community Banks Offer Personalized Service

Community Banks Offer Personalized Service

The choice to do business with a community bank is not just about the broader economy. When customers contact New Tripoli Bank, they are greeted by a talented team member who is attuned to their respective needs.

Community banks like New Tripoli Bank believe in building strong, long-term relationships with our customers through reliability, flexibility and goodwill. Because community banks serve a smaller geographic area than national banks, they are able to provide more flexible lending options for consumers and businesses, often assessing the broader picture of a person or organization’s financial situation, rather than just basing decisions off automated information, like credit scores.

Further, community banks also put a greater emphasis on maintaining long-standing relationships with their core depositors. While larger financial institutions seem to constantly change their service offerings in reaction to market trends, community banks focus on stability and reliability, which allows for them to plan for the future confidently. Making strategic decisions regarding lending and expansion is a component of that focus. This is one of the main reasons New Tripoli Bank has remained independent for 116 years.

Conclusion

We want to thank our customers for putting their trust in us for their banking needs. At New Tripoli Bank we pledge to never lose sight of the all-important relationships we hold and the personalized service our customers expect. Community banks are only successful if our customers and communities are, too. That’s why community banks and our relationship-based business model have thrived for over a century.

We know what it takes to create successful local economies. Join us in helping to build a vibrant economy here at home, in our community. We look forward to serving you soon.

Kayla Schnellman is the Client Services Lead for our New Tripoli Office. She has worked for New Tripoli Bank for over seven years, where she has worked as Community Banker, Customer Service Representative, and Head Teller. When she's not working, she enjoys spending time with friends and with her three dogs.

Kayla Schnellman is the Client Services Lead for our New Tripoli Office. She has worked for New Tripoli Bank for over seven years, where she has worked as Community Banker, Customer Service Representative, and Head Teller. When she's not working, she enjoys spending time with friends and with her three dogs.

New Tripoli Bank donated $11,000 to the Northern Valley EMS, Inc. (NOVA) in recognition of the important role the organization serves in protecting the health and safety of the communities they serve. John M. Hayes, New Tripoli Bank President and CEO, presented a check to Jason J. Breidinger, NOVA Public Relations Co-Chair, and Kristie Wentling, NOVA Executive Director, at the Bank’s New Tripoli office on Monday.

“NOVA plays a critical role in the safety of our community, and our donation shows the Bank’s faith in the service their employees and volunteers provide,” said Hayes. The Bank has shown its support for NOVA for many years through annual donations to their organization.

NOVA provides non-profit emergency medical services to North Whitehall, Washington, Heidelberg, and a portion of Lowhill Townships and the Boroughs of Slatington and Walnutport, serving more than 45,000 residents of the Lehigh Valley. They operate year-round, 24-hour ambulance services as well as providing emergency response training and education programs to volunteers in the community.

Payment cards are exceptionally convenient for consumers, and they come in various types –ATM, credit, debit, EBT – that enable low-friction banking and shopping. You probably use more than one. But you may not be aware of the various scams and tools fraudsters use to steal your payment information at the terminal and convert it into a substantial payday. It only takes seconds to install a scam device, and they can be anywhere. Fortunately, it takes even less time to protect your ATM and payment card.

Scam Devices

Scam devices have been found on ATMs, Point of Sale (POS) terminals, gasoline pumps – everywhere people use a card to pay. These devices capture personal data and PINs via video, digital download, or wireless transmission to the scammer. For example:

- Pinhole cameras are installed to record PIN entries and are so small they’re hard to detect. Note that pinhole cameras may be placed anywhere on or near the machine.

- Skimmers installed in the terminal or over its reader steal credit/debit card data from the magnetic stripe or chip.

- Keylogging keypads are overlays that cover the real keyboard, used to record a customer’s keystrokes. If the criminal knows what you type, they know your PIN.

Protecting Your Payment Card

- Inspect ATMs, POS terminals, and other card readers for loose, crooked, damaged, or scratched parts. If you notice something suspicious, use a different terminal.

- Check for keylogging overlays by lifting the edge of the keypad – a gentle tug is all it takes.

- Prevent cameras from recording your PIN by shielding your entry with your hand. Keep in mind that a pinhole camera may be present anywhere on or around the terminal.

- If possible, use ATMs in well-lit, high-traffic locations. Machines are less vulnerable in places where someone might notice a threat actor tampering with them.

- Be especially alert for skimming devices in tourist areas, where card readers are used a lot.

- When possible, use debit and credit cards with chip technology rather than magnetic stripes, which are more vulnerable to theft.

- Avoid using your debit cards for multiple accounts – the compromise of one card gives criminals access to all the accounts. Use a credit card instead.

- Routinely monitor your card accounts to promptly identify any unauthorized transactions. If possible, set up email or text-message alerts to notify you of account transactions.

- Proactively review the account security options. You may be able to set up multifactor authentication or freeze an account between transactions. Such steps may seem inconvenient, but they significantly reduce the risk of financial losses.

- Never give your PIN in response to a call, text, or email. Organizations that have your information would not request your PIN. They use other means to authenticate your account. If you receive a request, look up the source’s website and contact them to check your account.

- Always use a strong PIN. Avoid using PINs that may be easily guessed, such as strings of the same or consecutive numbers (e.g., 11111 or 1234).

- Find out if your account will allow you to temporarily block or freeze transactions on the account.

Tips for Paying at the Pump

- Choose the fuel pump closest to the store and in direct view of the attendant. These pumps are less likely to be targets for skimmers.

- Run your debit card as a credit card. If that’s not an option, cover the keypad when you enter your PIN. You should also examine the keypad before use for any inconsistencies in coloring, material, or shape. These inconsistencies might suggest that a foreign device (keypad overlay) is present.

- Consider paying inside with the attendant, not outside at the pump.

- Tap the card instead of swiping or inserting it when paying at the pump (if the card and terminal allow for it). Tap-to-pay transactions are more secure and less susceptible to compromise.

What to do if You Are Scammed

- Contact your financial institution immediately if the ATM doesn't return your card after you finish or cancel a transaction. It may indicate a foreign device is in the card reader.

- If you suspect your card was compromised, immediately contact your state benefits agency or card issuer. Promptly change your PIN if any funds remain in your account.

If You’re a Victim?

Immediately change any passwords you might have revealed. Consider reporting the attack to IC3.gov and the police.

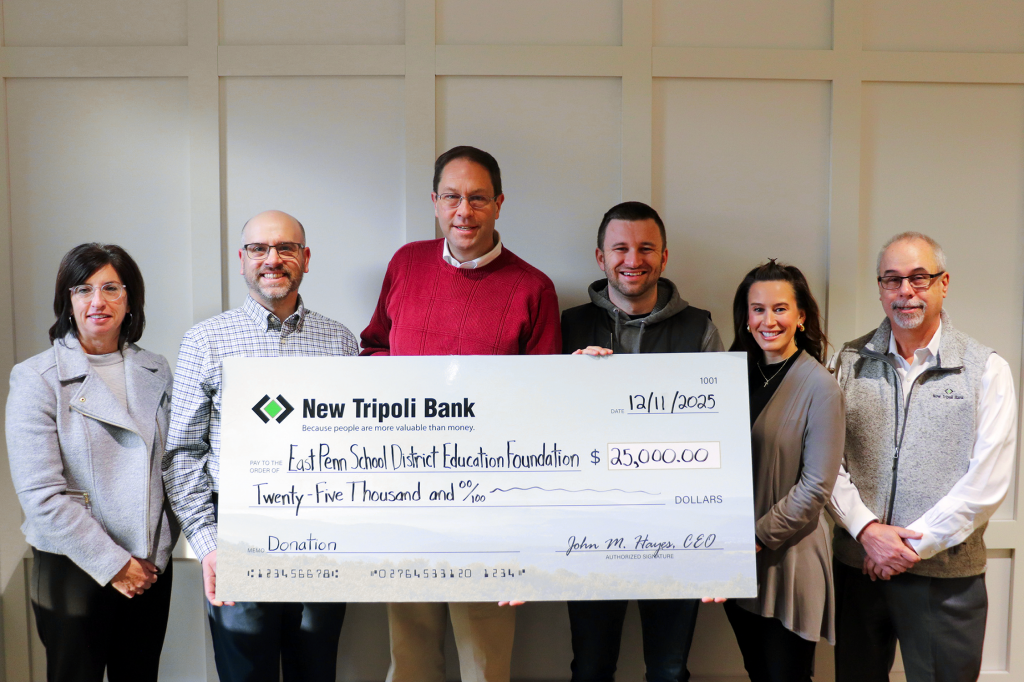

New Tripoli Bank has donated $25,000 to the East Penn School District Education Foundation to support approved educational needs in the District. These funds, which were supported by the Pennsylvania Educational Improvement Tax Credit program, will help the Foundation award grants for science, technology, engineering, arts, and math programs at schools throughout the East Penn School District.

A check for $25,000 was presented by John M. Hayes, New Tripoli Bank President and CEO, to members of the Education Foundation at New Tripoli Bank’s Buckeye Office. He presented the check to John Hemak, EPSD Education Foundation Treasurer and New Tripoli Bank VP and Commercial Lender, Kristen Campbell, Ed.D., EPSD Superintendent, Dr. Joshua Levinson, EPSD School Board Member, Jacob Reynolds, EPSD Education Foundation Director, and Dayne Buttafuoco, EPSD Director of Community Relations.

New Tripoli Bank is proud to have funded the EPSD Education Foundation for many years, as part of its continuing mission to support the community. This donation will be used to support EITC-approved programs that might not otherwise receive the necessary resources, furthering the Foundation’s mission to support STEAM education.

As a 115-year old business, history means a lot to New Tripoli Bank. We thought we should celebrate the history of our community by sitting down to interview members of our local historical societies and gather their perspective on history and its importance.

Their answers were varied, informative, and entertaining. We share them now with you as we prepare to celebrate the history of our nation on Thanksgiving. Hopefully this video conveys the importance of the work they do to preserve our history and celebrate it with future generations.

Many thanks to our participants!

- Albany Township Historical Society https://www.albanyths.org

- Emmaus Historical Society https://www.emmaushistoricalsociety.org

- Hivel Und Dahl Preservation Society https://www.hivelunddahl.org

- Lower Macungie Township Historical Society https://www.lmthistory.org

- Lynn-Heidelberg Historical Society https://www.lynnheidelberg.org

- Upper Milford Historical Society https://www.uppermilford.org

- Weisenberg/Lowhill Township Historical Society https://www.weisenberglowhill.org

Music used:

- "Country Blues Rock Ballad (Whiskey Moonlight)" Vlad Annenkov

- "Patriotic Medley March No. 2" Victor Military Band, Library of Congress National Jukebox

- "Ballin' the Jack" Victor Military Band, Library of Congress National Jukebox

- "Down Home Blues" Pennsylvanians, Library of Congress National Jukebox

- "A Day to Remember" Benjamin Tissot Bensound.com License code: Y8AQ5KRXWUUSFX5S

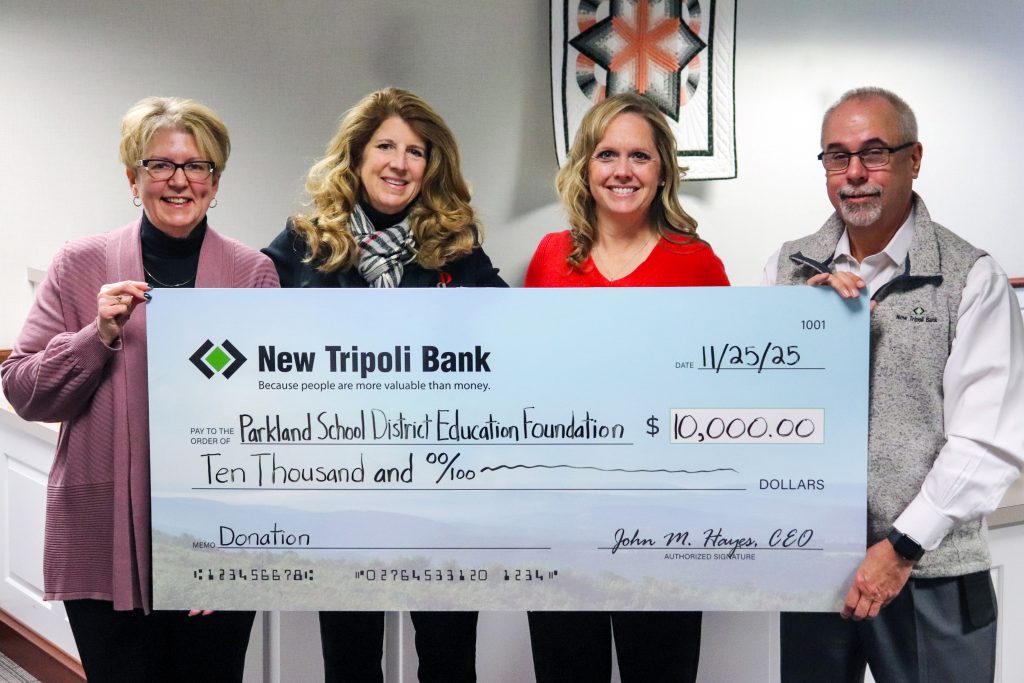

New Tripoli Bank has donated $10,000 to the Parkland School District Education Foundation to support approved educational needs in the District. These funds, which were supported by the Pennsylvania Educational Improvement Tax Credit program, will help the Foundation enhance educational opportunities for students across the Parkland School District through innovative programs, classroom resources, and unique learning experiences.

“Given the increased pressure on school districts and educators this year, it’s more important than ever to lend our support to important community organizations like the Foundation,” remarked John M. Hayes, New Tripoli Bank President and CEO. He presented the check for $10,000 alongside Michele M. Hunsicker, New Tripoli Bank Executive Vice President and Chief Financial Officer, to Lisa Ervin, Foundation Executive Director, and Christina Tori Morgan, Foundation President.

New Tripoli Bank is proud to have funded the Parkland School District Education Foundation for many years, as part of its continuing mission to support the community. This donation will be used to support programs that might not otherwise receive the necessary resources, allowing Parkland School District to allocate its funds in a way that leads to the best learning outcomes for its students.

by Tanya Hausman

I often spend time thinking about the best ways to prepare my children for the responsibilities of adulthood. Whether it’s teaching them the importance of proper hygiene, helping them learn how to manage their time between homework and social time, or encouraging healthy eating habits, I understand how vital it is that I be involved in their development.

One of the worries that I have personally experienced as a parent comes from my children having a debit card. Parents or guardians who have experienced a child begging for a brand-new iPhone or asking for money to go out with friends want that child to learn how to save money and spend it responsibly. Debit cards come with potential security risks on top of requiring some level of financial literacy.

Here are some tips to consider before letting your child have their own debit card.

Set Clear Rules

Before handing over the debit card, establish concrete guidelines for its usage. Discuss spending limits and clarify when and where you are comfortable with the card being used. Emphasize the importance of your child regularly checking their account balance before making a purchase.

Setting these rules in place at the start ensures less confusion later on.

Open a Linked Account

The best way to keep an eye on their spending habits is to link their checking account to your online bank account. This allows you to set spending limits and ATM access for children who are just starting to handle their own money, which gives them the freedom to use their debit card while putting restrictions in place.

Consider linking their account to your personal online banking account as it will also allow you to set up transfers between your other accounts and your theirs, making it easy to move money they earn from chores, allowance, etc. If they have a job, you can help them set up direct deposit into their account.

New Tripoli Bank customers can bring their children to any of our branches, and we’ll help to set all of this up!

Monitor Their Activity

Teaching children financial literacy and proper debit card use is a commitment towards long-term success. Once they have their own debit card, you’ll likely want to keep an eye on how they’re spending money. If you see them spending every dollar as soon as they get it, sit down with them and explain the importance of saving money for long-term goals, emergencies or just items that are important to them.

New Tripoli Bank’s online banking platform can help in this regard. You can add your child’s debit card to your account’s Card Secure and set up push or email notifications, so you are alerted whenever your child uses their card. Among other features, it also allows you to set restrictions on the card or deactivate it.

Teach Good Money Habits

It’s not enough to give your child the keys to their own finances; you need to show them how responsible adults budget their money. Most of a child’s learning comes from imitating those in their “money circle,” so it’s important to teach good habits.

Plan your monthly budget together. It’s important for children of all ages to learn concepts like income, expenses, and saving. If you’re currently saving up for a long-term goal, take the time to explain the budget process. Talk about how much you set aside each month, how you decided on that number, where you cut your other spending to save, and emphasize the importance of saving for the future.

Emphasize Security

A big part of using a debit card is making sure your personal and bank account information is secure. It’s critical they choose a strong, unique PIN for their debit card and go over emergency protocols in the event that the card is ever lost or stolen.

Customers at New Tripoli Bank can use the Card Secure feature on our online banking platform to monitor card activity. Take the time to go over their monthly bank statement together and explain how they can proactively identify potentially fraudulent transactions on their account in a timely manner.

Teach them the importance of online safety, whether it’s only buying from secure websites (look for “https” in the URL and a padlock symbol), avoiding entering personal information while on public Wi-Fi, or being able to identify scam ads and fraudulent offers on open marketplaces such as Facebook Marketplace.

Learning Through Experience

Mistakes on their journey to adulthood are likely. Use these mistakes as teachable moments instead. For example: if they overspend, spend some time talking about how it’s important to keep track of their account balances and avoiding impulse purchases.

As they become more comfortable using their debit card and show responsible habits, consider gradually loosening the controls you have on their card. This helps build trust between both of you and at the same time encourages them to continue practicing smart spending habits independent of your monitoring.

Tanya Hausman is a Senior Deposit Operations Specialist at New Tripoli Bank. She has been working for the Bank since 2014 in various roles. Outside of work, she spends her time baking, hobbying, and raising her two children.

Tanya Hausman is a Senior Deposit Operations Specialist at New Tripoli Bank. She has been working for the Bank since 2014 in various roles. Outside of work, she spends her time baking, hobbying, and raising her two children.

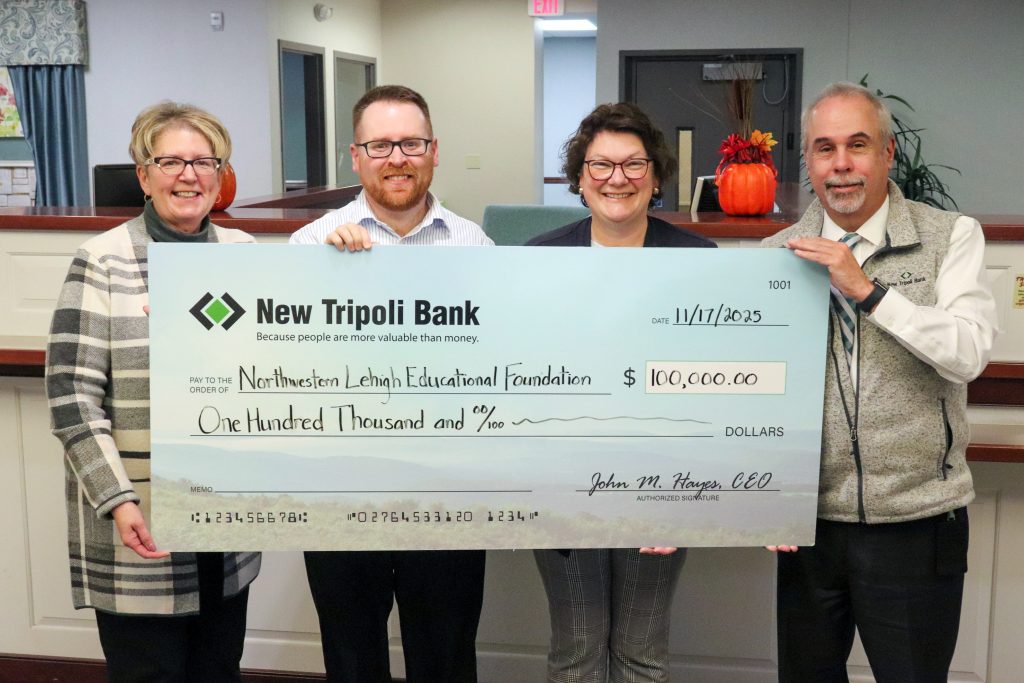

New Tripoli Bank has donated $100,000 to the Northwestern Lehigh Educational Foundation in order to support approved educational needs in the Northwestern Lehigh School District. These funds, which were supported by the Pennsylvania Educational Improvement Tax Credit program, will help the Foundation award grants for science, technology, engineering, arts, and math programs at schools throughout the Northwestern Lehigh School District. The Bank has been a proud supporter of NWLEF for over a decade, helping to fund modern teaching tools and classroom enhancements that empower Northwestern Lehigh students.

Regarding the donation, John M. Hayes, President and CEO of New Tripoli Bank, commented: “Our continued support is a testament to the lasting impact the Foundation has made on the outstanding learning outcomes of students at Northwestern Lehigh schools.” Hayes presented the check alongside Michele Hunsicker, Executive Vice President and Chief Financial Officer, to Matthew Koncz, NWLEF Treasurer and Board Member and Controller for New Tripoli Bank, and Amy Kinnon, NWLEF Development Director.

This donation will be used to support programs that might not otherwise receive funding, giving students in the Northwestern Lehigh School District the tools and skills they need to prepare for a career in a rapidly advancing world. New Tripoli Bank is a proud supporter of education, and this donation will ensure that our local school district remains at the forefront of technology enhancements that help prepare students for jobs upon graduation.

Due to the overwhelming response we received to last year's food drive, we are launching our Fall Harvest Food Drive early this year!

We want to make sure families in need in our area get the support they need this holiday season. Please bring your non-expired, non-perishable food items to any New Tripoli Bank branch by Saturday, November 29. We will be distributing your donations to:

- Bethel Bible Fellowship Church Groceries PLUS Food Bank: https://bethelbfc.org/outreach-ministries-1

- Christ's Church at Lowhill UCC Food Pantry: https://www.lowhillfoodpantry.com/

- Northern Lehigh Food Bank: https://mentalhealth.networkofcare.org/lehigh-pa/services/agency?pid=northernlehighfoodbank_2_794_0

- Parkland CARES Food Pantry: https://parklandcaresfp.org/

- Old Zionsville United Church of Christ Food Pantry: https://oldzionsucc.org/?page_id=136

We are accepting all donations, but the food pantries are especially looking for:

- Baked beans

- Canned beans

- Canned chicken

- Canned corn

- Canned fruit

- Canned green beans

- Canned peaches

- Canned pears

- Canned peas

- Canned Soup

- Canned vegetables

- Cereal†

- Chicken noodle soup

- Crackers

- Dry pasta

- Granola bars

- Jelly*

- Ketchup*

- Pancake mix† & syrup

- Peanut butter*

- Spaghetti sauce*

*Please only plastic jars/bottles, we cannot accept glass.

† Boxes preferred.

Effective immediately, we are unable to accept loose or wrapped pennies due to the Federal Reserve Bank restricting the supply of pennies.

The U.S. Department of the Treasury has officially ended production of the penny, which means New Tripoli Bank can no longer order pennies from or ship pennies to the Federal Reserve. We understand that this change will impact all of our customers and wanted to provide information on this shift in our monetary system.

Here are the main ways this change will impact our customers:

- We may not be able to do change orders that include pennies.

- You may be required to deposit your check if the change back to you would require pennies. You can then withdraw the cash that you need.

- For non-customers cashing a check drawn on New Tripoli Bank, you may be required to open an account if the change back to you would require pennies (exceptions may apply).

- Retailers and businesses may begin rounding cash transactions to the nearest nickel as pennies become unavailable.

Why is penny production ending?

The decision stems from the rising costs to produce new pennies. The current cost of the materials to create a new penny is almost four times the value of the currency, which in turn costs the government money each year.

Even though pennies are no longer being produced, existing ones are still legal tender. Here are some smart ways to transition away from using pennies:

- When paying cash at retailers, expect totals to be rounded to the nearest five cents.

- Consider switching to using digital payments or your debit card, which remain unaffected by the change.

- Sign up for direct deposit for paychecks and government benefit payments.